Towards 3% R&D – the role of industry policy by Roy Green

Today in our editorial series – Towards 3% R&D – Turbocharging Australia’s Innovation Effort – we turn to the role of national industry policy. Here Roy Green points to innovation and the success of a Future Made in Australia as intertwined.

While lacking detail at this stage, the significance of Prime Minister Albanese’s Future Made in Australia announcement should not be underestimated.

It is a timely recognition at the highest levels of government that ‘old orthodoxies’ have failed to shift the dial on stalled productivity, wage stagnation and energy transition.

The proposed legislation will not just be a tidy-up but a major change in the way Australia does innovation and industrial policy.

We now have the prospect of a more coordinated approach to the revival and reinvention of our manufacturing capability.

Clearly there are further steps to take, but already the current and former heads of the government’s own Productivity Commission, are engaging in an orchestrated campaign of criticism.

We have seen this criticism take a familiar form over the years, essentially that any attempts by government to reshape or diversify Australia’s narrow trade and industrial structure, based as it is on primary commodity exports, are bound to fail.

With a selective use of evidence and assumptions, it is said that such attempts would simply ‘encourage rent-seeking’, produce a ‘misallocation of resources’ and result in ‘sub-optimal outcomes’.

@AuManufacturing will publish contributions from readers for our series – Towards 3% R&D – turbocharging our national innovation effort – for the next month and in an e-Book, and we urge you to contribute. Call Peter Roberts, 0419 140679 or write to [email protected].

It is surprising that these claims are not more vigorously challenged by economists, as the Commission has itself – through relentless advocacy of privatisation, contracting out and other ‘reforms’ – enabled rent-seeking on a massive and unprecedented scale.

The result, as a series of public inquiries are now confirming, is not productivity-enhancing competition but innovation stifling market concentration.

Nor is the Commission averse to subsidies and tax concessions, provided they suit its doctrine of comparative advantage, which privileges the export of unprocessed raw materials over more complex, value adding activities.

Its annual Trade and Assistance Review regularly draws attention to what remains of the support for manufacturing while omitting any reference to fossil fuel subsidies.

For example, the diesel fuel tax rebate, which is accessed predominantly by a handful of international mining companies, costs the taxpayer $7.9 billion a year – more than half the entire Commonwealth spend on research and innovation.

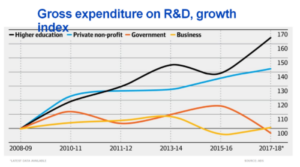

As a share of GDP, Australia’s R&D expenditure has declined to 1.68 percent, way behind the OECD average of 2.8 percent, with countries like Korea, Israel and Switzerland reaching 4 and 5 percent.

While the growth of business and government spending on R&D is at a standstill, universities have begun to do much of the heavy lifting, mainly as a result of their access to increasing international student fee income.

Clearly, this is not a sustainable proposition for the longer term. No wonder productivity growth in Australia, on the Productivity Commission’s watch over the last two decades, is the lowest for 60 years.

Hollowing out of manufacturing

The poet T S Elliot once observed that ‘humankind cannot bear too much reality’.

This is certainly the case when it comes to Australia’s ranking in the Harvard Atlas of Economic Complexity. The ranking, which measures the diversity and knowledge intensity of a country’s export mix, has continued its downward slide from around 55 in the 1990s to 93 today of 133 countries, just behind Uganda.

Some have questioned the methodology as it is focused on the composition of exports. Of course, in a globalised world, the value provided by exports is fundamental to national prosperity, but even if we discount this measure, another way of looking at Australia’s performance is with a location quotient (LQ) index devised by the Washington-based Information Technology and Innovation Foundation (ITIF).

This index identifies the share of advanced industries in the economy compared with its share of the global economy.

If Australia had the same share of advanced industry output as the global economy, its LQ would be 1.00. Such industries include pharmaceuticals, electrical equipment, machinery and equipment, motor vehicles, other transport equipment, computers and electronics, and information technology and information services.

In 1995, Australia’s advanced industries’ LQ was 0.56, meaning it had 44 per cent less advanced industry production as a share of its economy than the world.

But by 2018, its LQ had fallen to 0.41, ranking 51 of 74 nations, just ahead of Costa Rica and behind Iceland.

To compare, America’s LQ is 0.94, China’s 1.34, and Germany’s 1.74. Even the UK and Canada, which have also deindustrialised, lead Australia, with 0.80 and 0.60 scores.

The LQ for motor vehicles was just 0.13, which may be understandable with the closure of car assembly, but electrical equipment was 0.17 and machinery and equipment 0.20.

To compare, both Germany and Mexico have LQs of over 3.00 in motor vehicles, China and Korea have LQs of over 2.00 in electrical equipment, and Japan has an LQ over 2.00 in machinery and equipment.

If policy-makers want Australia’s advanced industry output to be the same share of its economy as the global average, output would have to increase by almost 1.5 times, or $105 billion.

Gaining share in advanced industries is critical because it means a larger economy, higher skill jobs and a more resilient and sophisticated industrial base.

The hollowing out of manufacturing, which together with related services drives research and skills development in most economies, has left Australia vulnerable to commodity price cycle and supply chain shocks.

In focusing on our comparative advantage in resources, policy-makers missed the chance to pursue new and existing areas of competitive advantage, based on knowledge and ingenuity.

Narrow trade and industrial structure

Some history provides the context. After starting at level pegging early last century, Australian living standards surged ahead of Argentina thanks to a crude but effective strategy of infant industry development behind protective tariffs.

The 1929 Brigden report noted that ‘the maximum income per head for Australia would probably be obtained by reducing it to one large sheep-run with the necessary subsidiary and sheltered industries’.

When by the 1980s, the costs of protection were seen to outweigh the benefits, the Hawke-Keating government embarked on a process of tariff reductions.

But in doing so, they introduced industry plans and structural adjustment measures to encourage a shift from vertically integrated mass production to smaller, more specialised firms that could compete in global markets and value chains, with increasing returns to scale.

While manufacturing as whole contracted, the success of this new approach could be gauged from the fact that ‘elaborately transformed manufactures’ became the fastest growing area of Australia’s export trade.

However, instead of building on this success in the subsequent commodity boom, governments complacently took the windfall gains and allowed the market to take its course.

As we now know, these windfall gains masked a deterioration in Australia’s productivity performance, as the ‘resource curse’ of a stronger dollar rendered much of the new manufacturing uncompetitive.

Rather than emulating the Norwegians, who took a stake in their North Sea oil and gas assets, imposed a 76 percent resource rent tax and created the world’s largest sovereign wealth fund, we followed the British model, which promoted short-term consumption over investment.

As a result, the manufacturing share of GDP in Australia is the lowest in the OECD at around 6 percent, with the manufacturing trade deficit doubling in the last two decades to $180 billion.

Essentially, iron ore and coal exports have enabled us to enjoy a developed economy lifestyle with a precarious underdeveloped industrial structure.

It seems extraordinary to international onlookers that the prospect of a future decline in these exports is not a matter of greater concern.

New approach to industrial policy

Nevertheless, Australia is uniquely fortunate, once again, in having another chance to get its policy settings right. And, faced with the existential challenge of climate change and energy transition, as well as the decline in global demand for our traditional exports, we must.

The scale of the opportunity is huge – to grow the industries and jobs of the future in a global market estimated to be worth $10 trillion by 2050.

Importantly, this opportunity must go well beyond switching reliance to new categories of raw materials, simply because they can be retitled as ‘critical minerals’.

For example, Australia currently produces 50 percent of the world’s lithium and sells 90 percent of it to China, but captures only 0.53 percent of its final value. It changes nothing in Australia’s domestic economy if these exports are redirected to other, more ‘friendly’ countries.

The Future Made in Australia initiative is the first step in a coordinated ‘whole of government’ approach to enabling competitive advantage in a new, higher value adding growth market for entrepreneurial Australian firms.

It will require close collaboration by industry with research and education institutions, including CSIRO, which can and do play a major part in lifting innovation and enterprise capability.

This approach also calls for a central institutional focus in the design and implementation of a mission-led, evidence-based industrial strategy, with national missions identified through regular technology foresighting and review.

Examples of such a focus include Vinnova in Sweden and InnovateUK, whose impact may be enhanced by a tripartite structure involving both industry and unions, as was the case during the Hawke-Keating period.

Clearly, there are many levers to be pulled as part of this strategy, including the newly established National Reconstruction Fund and Industry Growth Program, together with longstanding programmes such as the Industry Capability Network and Cooperative Research Centres.

The role of the R&D Tax Incentive, which absorbs an increasing proportion of the research and innovation budget, is due for rethinking in the context of more directly targeted programme.

In addition, there is scope for a more ambitious approach to public procurement, skills upgrading and the development of a network of place-based innovation ecosystems, which would complement conventional research commercialisation pathways.

Again, the design of this network can draw upon international experience, in particular the German Fraunhofer Institutes, UK High Value Manufacturing Catapults and US National Science Foundation Regional Innovation Engines.

There is now broad recognition around the world that government must play an active role in building a more inclusive and dynamic knowledge-driven economy, particularly with increasingly interconnected productivity and climate challenges.

Key to addressing these challenges is the need to grow manufacturing capability. Instead of telling us why the future cannot be made in Australia, the critics might more profitably turn their minds to how it can.

Further reading:

Towards 3% R&D – Boosting industry and research collaboration, by Dr Tony Peacock

Towards 3% R&D – The Statistics Do Not Lie By Dr John Howard

Emeritus Professor Roy Green AM is Special Innovation Advisor at the University of Technology Sydney and a member of the Board of CSIRO.

This series is brought to you through the support of our principal sponsor, public accounting, tax, consulting and business advisory BDO, and R&D tax incentive consultancy Michael Johnson Associates.

![]()

Picture: Professor Roy Green

Graph: Roy Green/Australian Bureau of Statistics

Topics a Future Made in Australia Analysis and Commentary arvard Atlas of Economic Complexity Athony Albanese computers Cooperative Research Centres CSIRO diesel fuel tax rebate electrical equipment electronics Future Made in Australia Industry Capability Network industry policy Information Technology and Innovation Foundation innovation machinery and equipment Manufacturing News motor vehicles national reconstruction fund other transport equipment pharmaceuticals Productivity Commission Professor Roy Green R&D tax incentive Technology the Industry Growth Program Towards 3% R&D towardsthreepercent Trade and Assistance Review

More in this section

@aumanufacturing Sections

Analysis and Commentary Awards Defence Manufacturing News Podcast Technology Videos